Millions of eligible borrowers won’t be able to benefit from the recent student loan forgiveness initiative. What options are still available?

In a landmark decision on June 30th, 2023, the Supreme Court struck down the Biden Administration’s federal student loan forgiveness initiative. It aimed to eliminate up to $20,000 in federal student loan debt for 43 million Americans who borrowed funds to attend college. U.S. Department of Education had previously stated that the student loan payment pause, which had been implemented during the COVID-19 pandemic, would expire on June 30.

So, the answer to the question “When will student loan forgiveness be applied?” is not in the nearest future. When do student loans resume? According to the ruling, millions of borrowers will have to begin repaying their loans in full starting September 1st. While interest rates were set at 0% during the payment pause, they will return to their current fixed rates once repayment begins.

If you’ve been looking forward to a favorable decision and now feel disappointed, you’re not alone. In this blog post, we’re reviewing the latest updates on the student loan forgiveness initiative and taking a look at the current student loan forgiveness programs.

Student Loans—Brief Overview

According to the data of the Education Data Initiative, “The average public university student borrows $25,969 to attain a bachelor’s degree.“

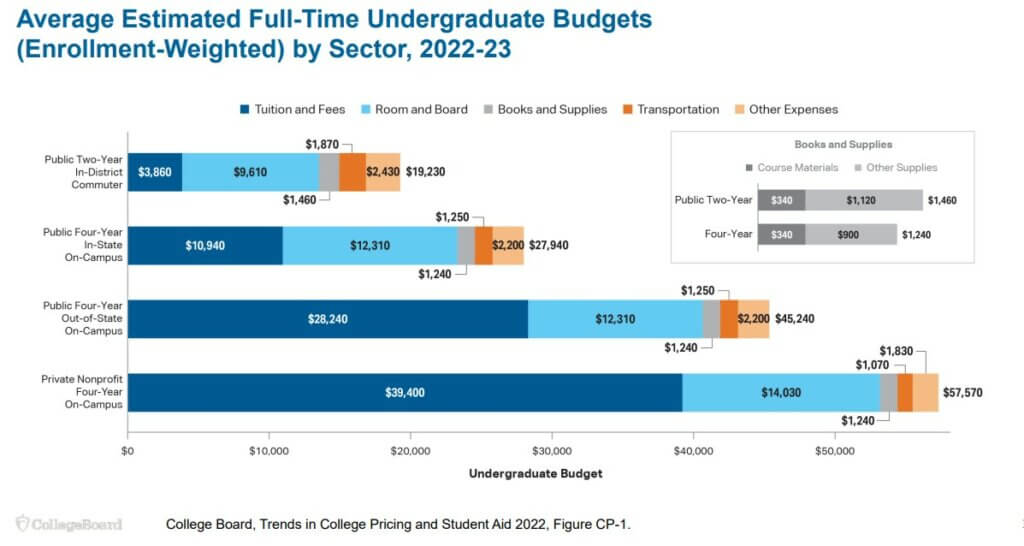

All in all, the overall state of student debt hasn’t changed for good in the past years. Since 1980, the total cost of both four-year public and four-year private colleges has nearly tripled. Here’re the College Board’s Trends in College Pricing 2022 report (p. 3) data regarding the average college budget of an undergraduate student:

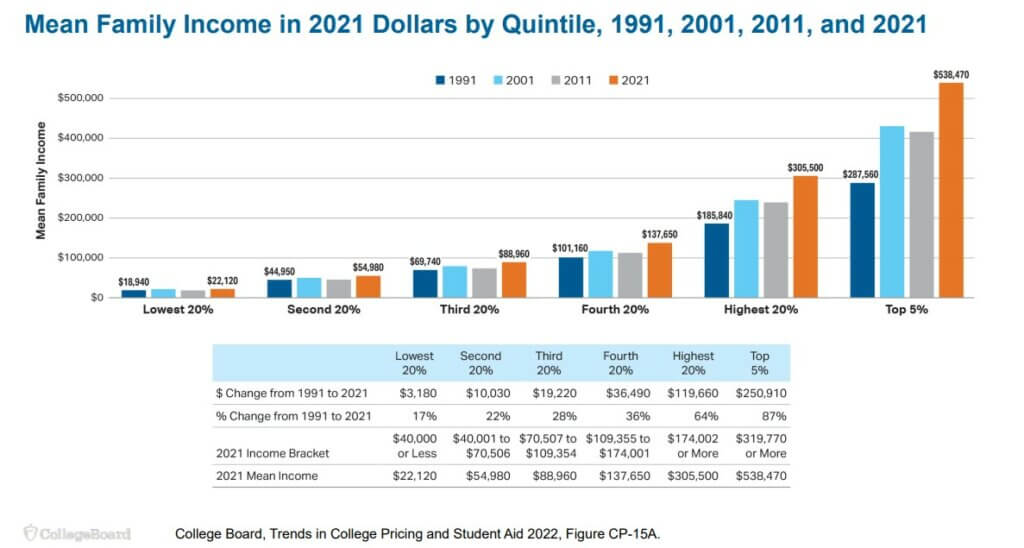

And here’s the overview of mean family income for the past thirty years (on the example of several groups depending on their earnings) from the Trends in College Pricing 2022 report (p. 21):

With so many families from the first few groups and average college budget prices being as they are, it’s understandable why the student loan forgiveness initiative was so anticipated. Many people can’t get over their student debt long after they’re out of college.

The Biden Administration’s student loan debt relief plan aimed to provide assistance to borrowers and families who were recovering from the pandemic and preparing to resume student loan payments in January 2023. The majority of the relief dollars, almost 90%, were supposed to be given to those who earned less than $75,000 per year.

The initiative wasn’t focused on individuals or households in the top 5% of incomes. By focusing on borrowers with the highest economic need, the initiative was expected to reduce the racial wealth gap, as Pell Grant recipients made up the majority of Black and Latino undergraduate borrowers, with 71% and 65%, respectively. However, once it failed, things are bound to get back to where they were (or get worse for some families).

Federal Student Aid

There’re several types of federal student aid options: federal grants (e.g., the Pell Grant), loans (including PLUS loans), work-study jobs, and other options that can help fund education.

High educational institutions across the country participate in federal student aid programs.

They use the information on the Free Application for Federal Student Aid (FAFSA®) form to determine a student’s eligibility for the Pell Grant and the amount they’re eligible to receive. Pell Grant amounts can change yearly.

| “The maximum Federal Pell Grant award is $7,395 for the 2023–24 award year (July 1, 2023, to June 30, 2024).” |

Federal student aid from the U.S. Department of Education usually covers the following expenses:

- Tuition and fees

- Housing and food

- Books and supplies

- Transportation

- In some cases, a computer and dependent care

How to Get Federal Student Aid

To apply for any student aid and stay eligible for it, you have to fill out a Free Application for Federal Student Aid (FAFSA®) form (and do it every year while you’re in school). You can use the form on Studentaid.gov to apply for federal student aid—grants, work-study jobs, and loans (e.g., student loan debt relief application).

However, looks like federal support has fallen behind: previously, Pell Grants used to fund almost 80% of the expenses of a four-year public college degree for students from working families, but presently, they only cover one-third of the cost. This has compelled numerous low- and middle-income families to borrow money if they want to pursue a degree. As per an analysis done by the Department of Education, the average undergraduate student with loans now completes their degree with a debt of almost $25,000. (Backed by the data from the Education Data Initiative we’ve referred to earlier.)

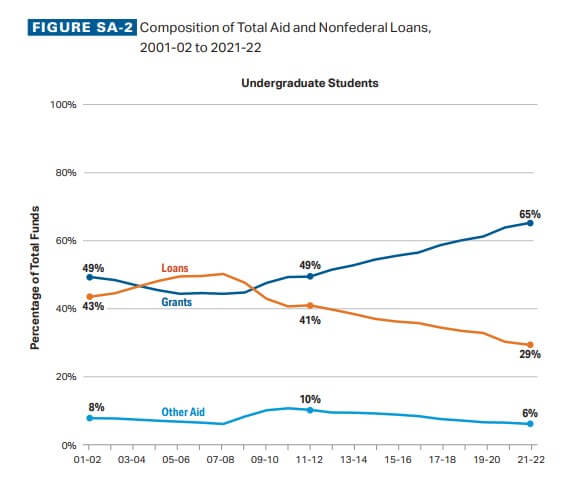

At the same time, during the past years, total grant aid for undergraduate students increased by 5%, and total loan volume fell by 43% between 2011–12 and 2021–22. Total grant aid for graduate students increased by 14%, and total loan volume fell by 9% between 2011–12 and 2021–22 (Trends in College Pricing and Student Aid 2022 report, p. 33).

According to the College Board (Trends in College Pricing and Student Aid 2022 report, p. 31) data, “In 2021-22, undergraduate and graduate students received a total of $234.6 billion in student aid in the form of grants, Federal Work-Study, federal loans, and federal tax credits and deductions.”

Student Loan Forgiveness

So as you can see, regardless of Biden’s student loan forgiveness initiative failure, there’re options to get financial aid and ways to get student loan debt forgiveness.

But before we take a look at those options, let’s analyze overall student loan forgiveness statistics for the recent period. According to the data of the Education Data Initiative, “Prior to 2021, just 6.7% of eligible borrowers applied for loan forgiveness; less than 0.3% of student loan debt was eventually forgiven.” After 2021, the total dollar amount forgiven was less than 0.6% (which is a bit higher than before). Also, here’re other data that help make a better picture:

- “Among processed applications for Public Service Loan Forgiveness (PSLF), 2.16% have been accepted since November 2020.

- Among denied claims, 30.7% are denied due to incomplete paperwork.

- 35.2% of PSLF applications have yet to be processed.

- A total of $34.309 billion in federal student loans have been forgiven through PSLF.

- Up to 10,100 teachers have successfully had their student loan balances partially or totally forgiven through the Teacher Loan Forgiveness Program.

- A total of $197.3 million in federal student loans have been forgiven through Teacher Loan Forgiveness.”

So, there’s a chance, isn’t there? You can still consider student loan forgiveness options (even though Biden’s plan is no longer one). These options primarily depend on your employment, income, the type of student loan you have, and the repayment plan you’ve chosen (Check the official Student Loan Forgiveness page on Federal Student Aid, the U.S. Department of Education for more details):

- Income-Driven Repayment Plans: These plans (such as PAYE, REPAYE, IBR, and ICR) cap your monthly loan payments. If you make these capped payments for a certain period (usually 20–25 years), the remaining balance of your loans will be forgiven.

- Public Service Loan Forgiveness (PSLF): If you work full-time for a qualifying employer (e.g., government or not-for-profit organization), you may qualify for forgiveness of the remaining balance of your loans after you have made 120 qualifying payments.

- Teacher Loan Forgiveness: If you have been employed full-time in a low-income school or educational agency for five consecutive years and have Direct and/or FFEL Loans, you may be eligible for loan forgiveness of up to $17,500.

- Loan Forgiveness for Nurses and Doctors: There are several programs that offer loan forgiveness for nurses and doctors who work in high-need areas.

- Loan Forgiveness for Military Personnel: Each branch of the military has its own student loan forgiveness program (e.g., the Army’s Loan Repayment Program can pay off up to $65,000 of student loans).

- Loan Forgiveness for Lawyers: Some law schools offer loan repayment assistance programs (LRAPs) to their graduates, and the Department of Justice has a loan repayment program for its attorneys.

- Perkins Loan Cancellation: Perkins Loan borrowers can have up to 100% of their loans canceled if they work in a public service job for a certain amount of time (usually five years of full-time employment).

- Closed School Discharge: If you withdraw from school or your school closes while you are enrolled, your federal student loans may be discharged.

- Total and Permanent Disability Discharge: If you’re totally and permanently disabled, you may qualify for a discharge of your federal student loans.

How to Apply for Student Loan Forgiveness

Here are the general steps to apply for student loan forgiveness:

- Determine your eligibility: There are different student loan forgiveness programs available, and each has its own eligibility requirements. Research and determine which programs you may qualify for.

- Complete the necessary paperwork: Each program has its own student loan forgiveness application process and paperwork requirements. You must complete the paperwork accurately and provide all the required documentation. (Remember the 30.7% denied-due-to-incomplete-paperwork cases we quoted earlier in this post?)

- Submit your application: After completing the paperwork, submit your application to the appropriate entity. Some programs may require you to submit your application to the Department of Education, while others may require you to submit it to your loan servicer.

- Wait for a decision: The student loan forgiveness process can take time, and it may take several weeks or months to receive a decision on your application.

- Continue to make payments: Until your application is approved, you should continue to make your monthly loan payments. By not doing so, you may default on the loan, which can have very serious consequences.

Student Loan Calculator

To understand how to repay your loan faster (or how to take a loan on the best terms if you’re considering one), you can use one of the student loan calculators. These tools help students and their families estimate the costs and repayment options of borrowing money to finance higher education. They usually take into account factors such as tuition fees, interest rates, loan terms, and the expected family contribution. Using this information, you can calculate the amount you might need to borrow and your potential monthly repayments after graduation.

Here are some examples of student loan calculators you can find online:

- Loan Simulator is an online tool the U.S. Department of Education provides to help students and borrowers navigate the complexities of student loans. It offers a range of features designed to calculate student loan payments and guides you in selecting the most suitable repayment options.

- College Cost Calculator: This calculator helps prospective students estimate the total cost of attending a particular college or university. It takes into account factors such as tuition fees, room and board, books, and other expenses.

- Loan Repayment Calculator: This calculator is designed to help estimate monthly loan payments based on the loan amount, interest rate, and repayment term. It allows you to experiment with different scenarios, such as variable interest rates or different repayment plans like standard, income-driven, or graduated repayment.

- Student Loan Refinancing Calculator: A refinancing calculator is great if you have existing student loans or student loan debt. It helps you evaluate the potential savings and benefits of refinancing your loans. Your current loan details, interest rates, and desired new loan terms can be entered to determine how much you may save when refinancing.

- Loan Consolidation Calculator: This calculator focuses on loan consolidation, allowing you to see the potential benefits of combining multiple loans into a single new loan.

- Income-Driven Repayment (IDR) Calculator: IDR calculators are specifically tailored to borrowers considering income-driven repayment plans. These calculators take into account your income, family size, and other factors to estimate your monthly payments under different IDR options.

These are just a few examples of the various student loan calculators available. Each one serves a specific purpose, aiding students and borrowers in making informed decisions about their education financing and student loan repayment strategies.

Conclusion

With all this being said, we can only conclude that while President Joe Biden’s still making plans to pursue another pathway to provide some student debt relief and protect borrowers, “This fight is not over,” we can only wait and see and rely on the already existing and available student financial aid programs and loan forgiveness options. Maybe, the next initiative will be more successful.